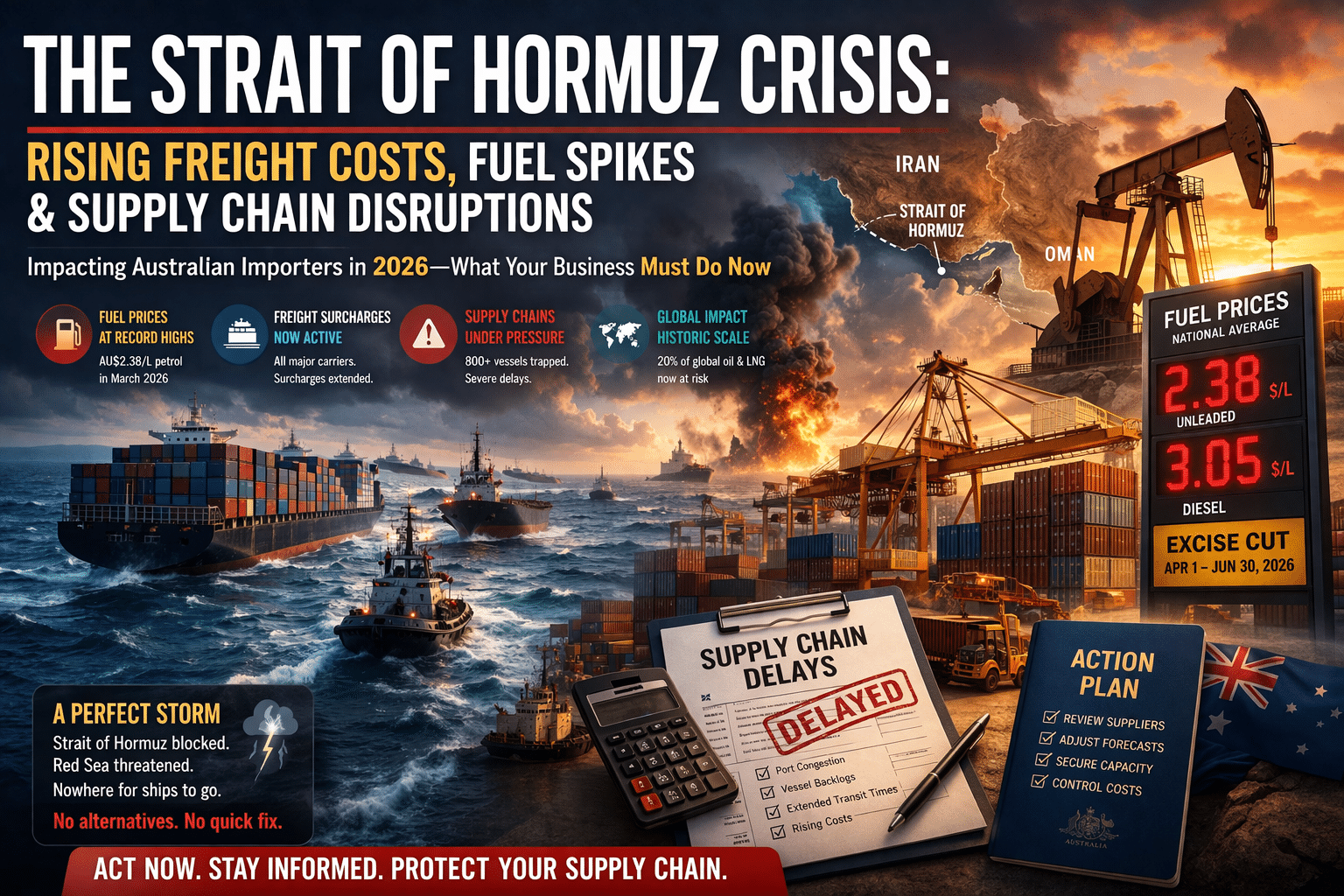

The Strait of Hormuz crisis, which began on 28 February 2026, has fundamentally changed the cost and complexity of importing and exporting goods for Australian businesses. Following joint US and Israeli military strikes on Iran — including the killing of Supreme Leader Ali Khamenei — the world’s most critical energy chokepoint has been effectively closed to commercial shipping for over five weeks.

A fragile US–Iran ceasefire was announced on 7 April 2026, but as of the time of writing, the Strait remains largely blocked. Only a handful of vessels have transited since the agreement, and Iran’s state media has indicated that tanker passage will remain restricted. More than 800 vessels are still trapped inside the Persian Gulf. The situation is highly fluid.

Emergency fuel surcharges from all major carriers on Australian trade lanes are already live — and have been extended beyond their initial expiry dates. Domestic fuel prices surged to record levels in March before a temporary government excise cut provided partial relief. And for the first time in modern history, both of the Middle East’s major maritime corridors — the Strait of Hormuz and the Red Sea / Bab al-Mandeb — are simultaneously disrupted, with Iranian allies threatening to close the latter as well.

This article explains what is happening, what it means for your supply chain, and the concrete steps Australian importers and exporters should take right now.

The Strait of Hormuz is a narrow waterway between Iran and Oman, roughly 33 kilometres wide at its narrowest point. Despite its modest dimensions, it is the single most important energy chokepoint on earth. Approximately 20 million barrels of oil transit the Strait daily — roughly 20 per cent of global seaborne oil trade — along with around 20 per cent of the world’s liquefied natural gas (LNG) supply.

For most countries, disruption to the Strait means higher energy prices. For Australia, the consequences are more acute. Australia imports over 80 per cent of its liquid fuel — refined petrol and diesel — primarily from refineries in Singapore, South Korea, Japan, India, Malaysia, and China. Those refineries, in turn, rely heavily on crude oil from Gulf producers including Saudi Arabia, the UAE, Iraq, and Qatar. When the Strait closes, the entire refining supply chain that feeds Australia’s fuel bowsers tightens simultaneously.

Unlike the Red Sea disruptions of 2024–25, which could be partially mitigated by rerouting vessels around Africa, the Strait of Hormuz has no viable alternative. There is no bypass. Cargo trapped in the Persian Gulf simply cannot get out.

The immediate trigger was a joint US–Israeli military operation targeting Iran on 28 February 2026. Iran’s Islamic Revolutionary Guard Corps (IRGC) responded swiftly, declaring the Strait closed and warning that any vessel attempting to transit would be attacked. By 12 March, Iran had carried out at least 21 confirmed attacks on merchant ships and over 150 tankers anchored outside the Strait in the Gulf of Oman, unable to enter or exit the Persian Gulf.

The scale of the shutdown has been unprecedented in modern history. Shipping traffic through the Strait dropped from approximately 105–135 daily transits before the Strait of Hormuz crisis to fewer than 13 by early March — just 8 per cent of normal volume. According to visibility platform project44, more than 34,000 ships had diverted their routes in the first four weeks of the disruption alone, with no sign of normalisation. Major carriers including Maersk, MSC, CMA CGM, and Hapag-Lloyd suspended all transits almost immediately. As of early April, more than 800 freighters remain trapped inside the Gulf.

On 27 March, the IRGC formally tightened the closure, banning passage for vessels going “to and from” ports of the US, Israel, and their allies. The US military launched a campaign to reopen the Strait on 19 March. A fragile two-week ceasefire between the US and Iran was announced on 7 April, but within hours Iran halted tanker passage again, citing Israeli attacks on Lebanon. The situation remains unresolved.

Compounding the Strait of Hormuz crisis, a top adviser to Iran’s new Supreme Leader has threatened to close the Bab al-Mandeb strait as well — which would block a quarter of global energy supply simultaneously. The Houthis in Yemen have already signalled their readiness to resume attacks on Red Sea shipping. If both corridors are effectively closed at once, the impact on Australian supply chains would intensify substantially.

Brent crude oil prices surpassed US$100 per barrel on 8 March 2026 for the first time in four years, reaching a peak of US$126 per barrel. By early April, Brent had moderated to around US$104–110 per barrel, though analysts warn that a breakdown in the ceasefire could drive prices toward US$150 per barrel or higher. The head of the International Energy Agency has described the blockade as more consequential than the oil shocks of 1973, 1979, and 2022 combined.

The consequences for Australian consumers and businesses have been rapid and severe. National average unleaded petrol prices hit a record AU$2.38 per litre in late March 2026 — a jump of approximately 50 cents per litre in under a month. Diesel surpassed $3 per litre in multiple capital cities through March.

In response, on 30 March 2026, Prime Minister Anthony Albanese announced the temporary halving of the fuel excise, effective 1 April to 30 June 2026, at a total budget cost of approximately $2.55 billion. The ACCC was tasked with monitoring that the saving was passed on at the bowser. As of early April, national average unleaded prices have moderated to approximately $2.35–2.45 per litre following the excise cut — but diesel has shown less relief and continues to threaten new highs, with some stations already exceeding $3 per litre. Diesel shortages have been reported at approximately 3–4 per cent of stations nationally.

Even with the excise cut, fuel prices remain 20–40 per cent above pre-conflict levels. Analysts at Westpac have warned that headline inflation could reach 5.5 per cent year-on-year by mid-2026, driven significantly by fuel. Treasury modelling suggests a prolonged oil shock could shave 0.6 per cent or more off GDP in 2027.

Australia’s fuel security position makes it uniquely exposed. As of late March 2026, Australia held approximately 36 days of petrol supply, 32 days of diesel, and 29 days of jet fuel in reserve — among the lowest strategic stockpiles of any IEA member nation against the IEA’s 90-day requirement. The government has confirmed that several oil shipments originally bound for Australia were turned back or deferred in March and April. Diesel — the lifeblood of the freight and agriculture sectors — remains the most vulnerable supply.

The impact on the cost of moving cargo to and from Australia is immediate and compounding. Every major shipping line on Australian trade lanes — including CMA CGM/ANL, Hapag-Lloyd, MSC, Maersk, OOCL, ONE, PIL, SeaLead, Evergreen, and others — has implemented Emergency Fuel Surcharges (EFS) or Emergency Bunker Surcharges (EBS). All 15+ carriers serving Australian trades are now charging these surcharges on every trade lane.

Key surcharges in effect include:

It is critical to understand the mechanism here. These surcharges are not limited to vessels sailing through the Persian Gulf or the Red Sea. Marine fuel is a globally priced commodity. When oil prices rise, the additional cost flows through to every trade lane worldwide — including Australia–China, Australia–USA, and intra-Asia routes that never go near the Gulf. The Hormuz blockade has effectively levied a tax on all international freight.

Importers and exporters should also be aware that rerouting vessels around the Cape of Good Hope adds approximately 3,500–4,000 nautical miles and 10–14 additional days of transit time to Australian–Europe, Australian–Middle East, and Australian–UK lanes, compounding the cost pressure.

Beyond emergency fuel surcharges, Australian businesses face a cascade of additional costs:

War Risk Insurance Premiums War risk insurance premiums have increased dramatically — with rates reported to be four to five times pre-crisis levels. The Joint War Committee of the London insurance market has now included waters around Oman in its list of high-risk maritime areas, following drone strikes on the ports of Duqm and Salalah. Many standard maritime insurance policies include a 72-hour cancellation clause at the discretion of the insurer when conflict escalates, meaning coverage can evaporate with minimal notice.

Bunker Adjustment Factors (BAF) BAF surcharges are running at elevated levels across all trade lanes. Importers who locked in long-term freight rates without appropriate BAF clauses may face significant unexpected costs. Wholesale diesel in Australia has risen more than 67 per cent since early March; surcharges of 8–10 per cent are now appearing on building projects and freight contracts across the country.

Global Capacity Crunch and Schedule Reliability With over 800 vessels stranded inside the Persian Gulf and thousands more diverted around the Cape, the effective global fleet has shrunk and schedule reliability has deteriorated. Carriers are rolling containers at origin, blank sailings are increasing, and booking lead times have extended significantly.

Air Freight Disruption Emirates, Etihad, and Qatar Airways are still not operating normal schedules, reducing belly-hold capacity on Australia–Europe air freight lanes by approximately 18 per cent. Spot air freight rates to Europe are up more than 35 per cent since 1 March. For importers relying on air freight to bridge supply gaps created by the ocean disruption, this avenue is both more expensive and less available than usual.

Domestic Road Freight Costs Australian road transport consumes around 10–12 billion litres of diesel annually. Major operators including Toll, Linfox, StarTrack, and Australia Post have announced increased fuel surcharges in March and April. Businesses relying on domestic last-mile delivery are seeing these costs pass through now. The heavy vehicle road user charge has been reduced to zero until 30 June 2026 as part of the government’s excise relief package — providing some partial offset for fleet operators.

Australian importers who navigated the Red Sea crisis of 2024–25 may be tempted to apply the same playbook. This would be a mistake. The two situations are fundamentally different in scale and in the availability of solutions.

The Red Sea disruption had a bypass: vessels could reroute around the Cape of Good Hope, absorbing additional transit time and fuel costs but ultimately still moving cargo. The Strait of Hormuz has no equivalent alternative. Cargo stranded inside the Persian Gulf cannot be rerouted — it simply waits.

The energy dimension also distinguishes this crisis from all previous shipping disruptions. The Red Sea did not directly affect global energy supply. The Hormuz closure has removed approximately 20 per cent of global oil supply from the market — more than the 1973 and 1979 oil shocks combined, according to the IEA. That energy shock flows directly into the cost of running every truck, ship, and aircraft in Australia’s logistics network.

The potential closure of the Bab al-Mandeb in addition to Hormuz — now a credible rather than remote risk — would extend the disruption to a quarter of global energy supply simultaneously. There is no historical precedent for that scenario.

The current environment demands a different operating posture. “Just-in-time” logistics is not viable when both transit times and surcharge structures can change week to week. Synergy Freight recommends the following approach:

1. Audit Your Full Cost Exposure — Including Domestic Freight Map every freight cost in your supply chain — not just ocean freight. Review your domestic transport contracts for fuel levy clauses and trigger points. The fuel levy recalculation cycle has shortened to weekly for many operators. Businesses that understand their full exposure are better positioned to renegotiate, absorb, or pass through these costs strategically. Also pull your freight contracts and check force majeure provisions: in most standard Australian contracts, these protect the carrier, not the shipper.

2. Extend Your Inventory Buffer to 21+ Days The combination of vessel strandings, port congestion, Cape routing delays, and deteriorating schedule reliability means significant disruption to expected arrival windows. We recommend building a minimum of three weeks of additional buffer into all inventory planning. For businesses that rely on China, Southeast Asia, or any origin connected through Middle Eastern transshipment hubs, the risk of unexpected stock shortages is elevated heading into Q2 2026.

3. Review Your Incoterms, Contracts, and Insurance Cover. Scrutinise every active freight contract and purchase order. Confirm whether you or your supplier holds responsibility for freight costs under your agreed Incoterms — and whether war risk surcharges are included or excluded from your current pricing. Many importers are finding that costs quoted on a CIF or DAP basis are now subject to surcharges that were not anticipated when the contract was agreed.

Confirm your cargo insurance coverage explicitly covers the current Middle East risk, including the now-elevated risk zones around Oman. Do not assume existing policies remain valid without checking directly with your insurer.

4. Work With a Proactive Freight Partner In a crisis of this nature, the value of your freight forwarder extends far beyond booking containers. A proactive partner monitors carrier surcharge announcements in real time — many are now on weekly review cycles — identifies alternative routings before you ask, and flags documentation or compliance issues before they cause expensive delays.

If you haven’t already spoken with your freight partner about the specific impact on your upcoming shipments, that conversation should happen today.

The situation remains highly fluid. Key developments to monitor include:

Does the Strait of Hormuz closure affect my goods coming from China or the USA? Yes — even though those trade routes do not pass through the Strait of Hormuz, the global cost of marine fuel has risen sharply due to the energy shock and vessel disruption. Every major carrier has issued emergency surcharges on all trade lanes, including Australia–China and transpacific routes.

Why are my domestic Australian delivery costs increasing because of a Middle East conflict? Most of the refined petrol and diesel used in Australia comes from Asian refineries that rely on crude oil transiting the Strait of Hormuz. When the Strait is blocked, crude supply to those refineries tightens, pushing up the price of refined fuel. Australian road transport operators are passing those cost increases through emergency levies, which are now being reviewed weekly.

Are there alternative routes for ships that usually use the Strait of Hormuz? No — this is what makes the current crisis more severe than the Red Sea disruption. The Strait of Hormuz has no bypass. Cargo stranded in the Persian Gulf cannot be rerouted — it cannot exit until the Strait reopens. All vessels are currently routing via the Cape of Good Hope, adding 10–14 days and significant fuel costs to most Australian trade lanes.

A ceasefire was announced — does that mean the Strait of Hormuz crisis is over? Not yet. The 7 April ceasefire between the US and Iran is fragile and unverified on the ground. As of 8–9 April 2026, only a handful of vessels had transited the Strait and Iran’s media reported tanker passage remains blocked. More than 800 vessels remain trapped in the Gulf. Even if a genuine reopening occurs, supply chain normalisation — including insurance markets, vessel repositioning, and carrier surcharge cycles — takes weeks, not days. Businesses should continue to plan around disrupted conditions for the foreseeable future.

How long will the emergency fuel surcharges on Australian trade lanes last? Most current surcharges were originally filed with expiry dates in early to mid-April 2026 and are now being reviewed and extended. The Australian Treasurer and industry analysts have flagged 12–36 months of elevated prices as a credible planning horizon if the underlying geopolitical situation does not fully resolve. Synergy Freight will keep clients updated as carrier advisories are issued.

Should I be accelerating upcoming import orders? This depends on your specific situation — product type, cash flow, and storage capacity all factor in. If you have inventory that you know you will need and the cost of holding it is manageable, bringing forward orders is a sensible risk mitigation step. However, vessel space is constrained, schedule reliability has deteriorated, and booking lead times have extended substantially. Speak with your freight forwarder before committing to expedited bookings to confirm space and realistic arrival windows.

The 2026 Strait of Hormuz crisis has become the most significant disruption to global energy and freight markets in over fifty years. For Australian businesses, the combination of domestic fuel price shocks, emergency carrier surcharges, extended transit times, tightening vessel capacity, and a fragile and unresolved geopolitical situation demands an immediate and structured response.

A temporary ceasefire is not a resolution. Businesses that treat the current moment as a reason to pause rather than act will find themselves exposed when surcharge cycles reset, inventory buffers run low, and the next escalation — whether in Hormuz or Bab al-Mandeb — arrives without warning.

The businesses that will weather this period best are those that move now: reviewing their costs and contracts, extending their inventory buffers, checking their insurance, and working closely with a freight partner who has real-time visibility across the market.

Is your supply chain protected against the current Strait of Hormuz disruptions? Contact the team at Synergy Freight Management today for an emergency logistics health check.

📞 +61 410 355 355 | 🌐 synergyfreight.com.au/contact | Book a Discovery Call

Last updated: April 2026. Synergy Freight Management is a Sydney-based freight forwarding, customs brokerage, and logistics company serving Australian importers and exporters.

We understand you prefer to receive or ship your products without the hassle of managing the freight process. We're your freight partners. Your success defines our own.

Copyright © 2025 | Synergy Freight Management Services | Policies